The World of Life Insurance Part Two — The Next Generation?

Last month we featured guest Bobby Samuelson and Windsor's Marc Schwartz in a conversation about "The World of Life Insurance – Version 2023." In the course of that discussion, Marc and Bobby both touched on the recent introduction of Variable UL products based on the success of Registered Index Accounts, with Bobby saying "I'm excited to see how this corner of the market develops over time. It's nothing but positive for distributors, agents and consumers." Today's blog, originally a podcast, brings together Marc, Jeff Driscoll of NFP, and moderator Kristin Williams, NFP's Senior VP of Strategic Resources, to explore the impact and implications of these innovative new products in more detail.

Kristen Williams: I'm Kristen Williams, and today I am joined by Jeff Driscoll, NFP's Vice President of Product & Carrier Management, and Marc Schwartz, Principal at Windsor Insurance Associates and Managing Director of NFP Life Solutions. Marc and Jeff are here to talk about the new Indexed Universal Life (IUL) investment options inside a few recently introduced products: What that means for us, what it means for the industry, what it means for our more familiar IUL products. So, Marc and Jeff, thanks for joining us today.

Let's jump right in. Marc, for many years we've been able to invest in IUL options inside of the VUL contract. What makes these new products different? How did we get here? And where should we go? What should we expect to see going forward?

Marc Schwartz: This has really been an evolution that has grown out of the success of indexed annuities that offer new indexed options. Those products are called RILAs, registered indexed linked annuities, and that space has grown dramatically over the last four or five years, so that now there's billions of dollars of annuity premium going into products that have these unique index-linked options.

The carriers that have had success with RILAs drew that feature into the life insurance space. These options are different in the sense that — unlike a traditional IUL indexed option where they have the upside return capped, and a zero floor — these new options actually have a broader range of results, meaning that you can have losses: you can have a negative return. You can also have a higher cap. But as we'll get into in more detail, part of that loss is protected, but not all of it. And that's why they're registered variable products rather than fixed indexed universal life products.

Kristin: Okay. So those buffers that Marc was talking about, Jeff. How do those work?

Jeff Driscoll: These are indexed options that offer a higher upside. So either a higher cap rate or participation rate in exchange for the consumer accepting a downside risk.

For example, with Prudential's new product: The first 10% of the downside is protected. When you have a negative 12% loss, the account would only have a 2% loss. So you're buffered against the first 10% of loss..

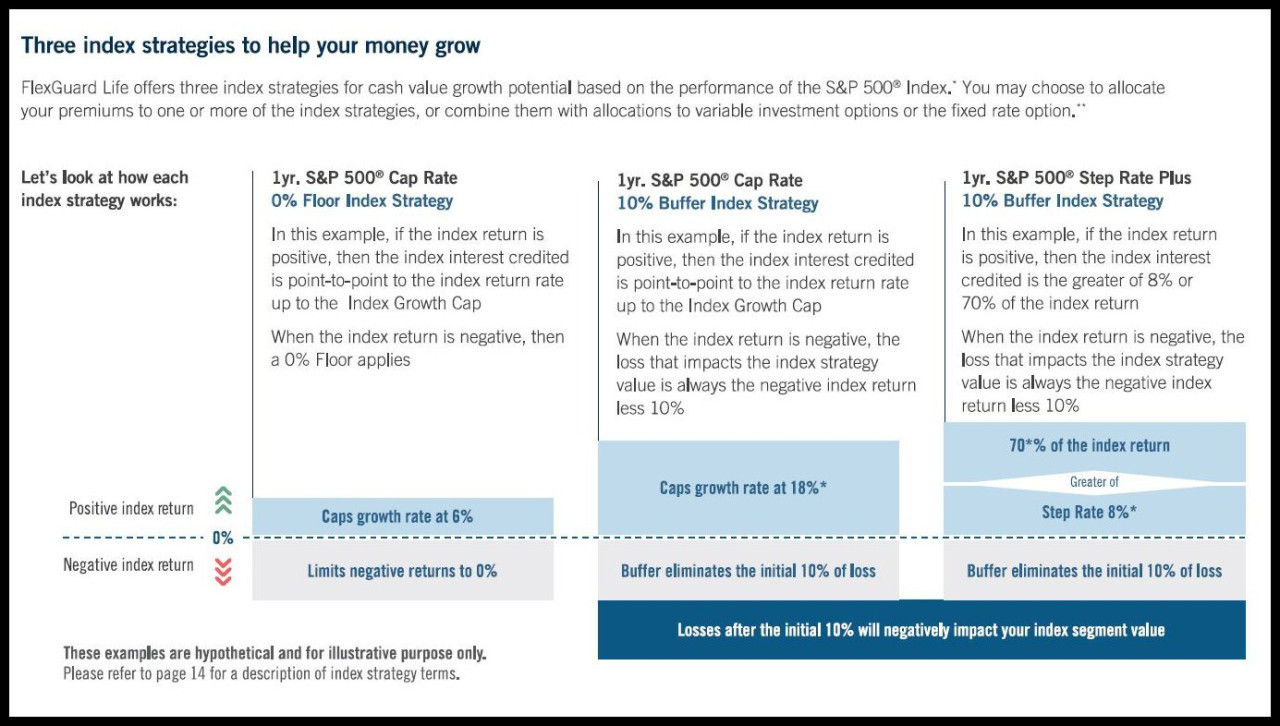

Kristin: And, Marc, the Prudential Flexguard product. What are the index options and buffering inside that product?

Marc: This is their first version of the Flexguard product, and they offer a traditional IUL option, point to point with a cap and floor. But the two new unique options are, first, a buffered S&P point to point where you have a high cap of 18%, and as Jeff mentioned, the first 10% of the downside is protected or buffered against loss. So really anything from a negative 10% up to a positive 18% is the range for that option.

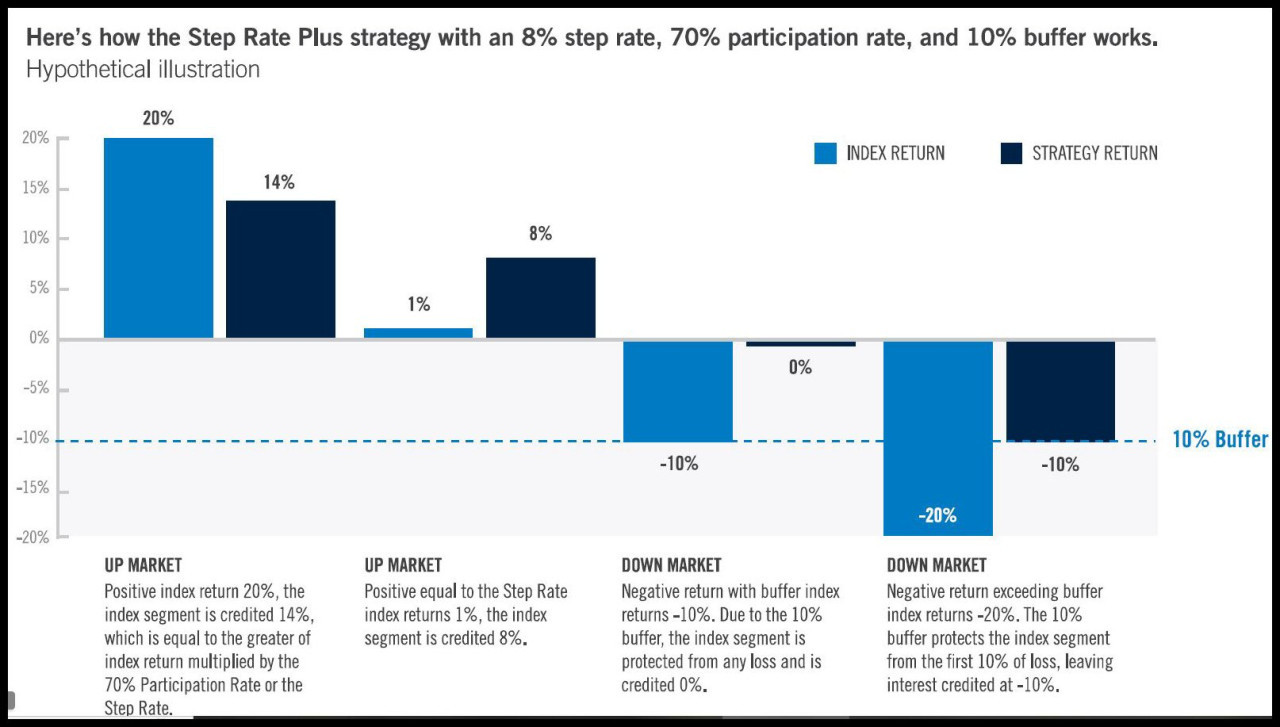

And then a second buffered account, which is a little different. They call it a buffer with a stepped S&P point to point, and the way this one works, if the return is anywhere positive from 0 to 8%, the client will get 8%. So you kind of think about that as a step rate, or a trigger. Anything positive within that range you're going to get 8%. But if it's higher than that, you'll get the higher return multiplied by the par rate, and their current participation rate is 70%. Those are the two buffered options that Prudential has, but they also offer a fixed account, and they also offer nine traditional, variable life sub-accounts as well.

Kristin: That sounds like a lot of different options. Jeff, when our audience gets super excited about these buffered accounts, and they call to ask for modeling help, how can we help them figure out which one to use over all the other options?

Jeff: It will take some explaining, right? Advisors will need to learn how the accounts work and where they fit on the risk spectrum. Let's just take the two buffered accounts from Prudential. The downside protection is the same. It's a 10% buffer on each of those accounts. But the upside credit and how it's calculated, that's what's different.

Let's take the account with the 18% cap rate. If the index returns a positive return, the policy only gets a credit up to a max of 18%. That's pretty straightforward.The step rate account, if that has a positive return between 0 and 8%, like Marc said, you get the 8%. However, if the return is subject to the 8% rate, the return is also subject to a participation rate of 70%.

So think of it this way: You would need a return of 11% or greater to get to 8%. That's sort of the break-even point to benefit above the 8% step rate. To keep it simple, if a client expects a return between 0 and 8%, they'd be better off in the step rate option, because they're automatically going to get 8%. And if there's an expectation that they'll earn above that, then they may be better off with the 18% cap option. And another way to look at it is, you would need a 26% return times the 70% participation rate to get 18%. So if you don't think you're going to get that, you may be better off with the step rate account.

Kristin: Okay, thank you, Jeff, that was a helpful way of putting it. Marc, you spoke about Prudential's Flexguard product. Are there any other RILA-type options in life products on the market now, and do you anticipate any other carriers will be getting into this space?

Marc: Equitable was really the first to bring this investment option into the market. They've had it for a number of years. And they also have a big RILA indexed annuity product out in the space. So I think the two of them, Equitable and Prudential, really are the primary carriers today that have come out with products. Pru is the new player on the block. There's a lot of promotion, a lot of interest going on with their product. Both Jeff and I have heard from several carriers that they're exploring adding these kinds of unique index options to their variable products or registered indexed universal products. So we do think there will be more over time.

As to whether or not carriers go down this path, I think they'll probably see how the market reacts, and, as we all know, everybody copycats pretty quickly. So if there's some success I think we should expect to see more of these options being offered.

Kristin: What do you think will happen to the market share for more traditional VUL, that maybe doesn't have the RILA, or even the IUL that we all have known and loved for so many years?

Marc: As you think about this, we keep segmenting the risk tolerance market tighter and tighter in our products, and it is an area where carriers can compete and offer something new. So, when Jeff and I were talking about this, I think it comes down to risk tolerance, kind of what's the client's perspective, right? If people were inclined to buy VUL, I think this is a really nice addition, because they're already willing to accept that downside risk. And now you can buffer some of that risk and still capture a very high rate of return. That's more than I would say you often need in a life insurance product to be successful. When you spin it to the IUL side, you do have the barrier there that you have to be licensed to sell these registered products, and so there are some producers who will not be interested.

But when you look at what's going on with the IUL market today, lower cap rates and lower illustrated rates and regulatory changes, with AG 49A, and the recently announced AG 49B. So we do think there's a chance that these products will take some market share from both sides, and in particular whatever product is competitive and offers a long duration guarantee. And it will be interesting, because you can get a lifetime guarantee, an age 100 guarantee, to see how that fits in the market and how the market reacts to it.

Kristin: It sounds like it might even be kind of a gateway into VUL for somebody who is interested in Variable Life, but wants a little bit more protection and sort of a buffer. It might be a way to ease into VUL, would you agree with that?

Marc: I agree. I think it's a great way of thinking about it. If you're not fully comfortable with all the downside you have in traditional VUL, this does give you a really nice option to have some protected return there.

Kristin: Jeff, one of the things I always love about talking to you about products and carriers is you're such a student of the industry and the carriers that you have great theories about why carriers might be likely to make X moves or introduce Y products. Do you have any theories about these RILA accounts, and why we see them with a couple of carriers, and may see more of them going forward?

Jeff: These specific carriers have seen great success on the RILA side, right? The marketing story resonates greatly with consumers. So they're counting on that success on the VUL side or index VUL side. I don't think it's more complicated than that. I don't think there's a man behind the curtain, right? I think this is where they've seen a marketing story play out well. Consumers like it, so they want to bring it on to the life side, the VUL side. And the other thing they can take advantage of, the carriers that have come out with it and carriers thinking about it, is that they have already have investment folks working with these options and hedging this way, and then calculating rates this way. Those carriers can take advantage of that experience.

But I don't think it's going to be an overnight success, because carriers often have different wholesalers on the annuity side versus the life side. So it will still have a learning curve. But I think the reason they've made the investment is that the marketing story is a really good one.

Kristin: Okay, that's great. Marc, as you know, life insurance is the answer to all the questions, and we're just talking about how maybe these new options can offer a gateway into VUL. Where do you see these products really singing? What type of client profile, if we do an "I got a guy," what does that guy look like?

Marc: Good question. Looking at them currently, and particularly the Pru product, I think our marketplace is going to see it as an additional option for the long-term duration guarantees sale, and we know that a lot of those sales have moved to the VUL chassis already. The marketplace is already comfortable with it. We see that in the success of Pru's VUL Protector and Lincoln's product, and in Penn Mutual and Securian, among others. So I think you have a good base of people who are going to view this as "another one I need to be pricing for long duration guarantees."

From what we can see initially, single premiums look good, at least relative to Prudential's other alternatives, and I think we'll learn more about that. Death benefit options or death benefit long term durations are one place this fits. But the other place — and this will take longer, I think, and we don't do as much of this — is the LIRP sale, where there's a bit of a growing VUL, or return to VUL, kind of coming back to the nineties, with a Life Insurance Retirement Plan type of sale. And when you think about it, this is the better product for that in a sense, because you have all this optionality, and if someone keeps it all the way to retirement and they're taking out cash flow from this policy, now you have an option that protects your downside to some degree, but still gives you a market return, you know, 7, 8, 10, 12 percent, if the caps are still that high. You can potentially get a really nice return. So, in that phase when money is coming out of products, this could be a really nice product for that. But I think it'll take some time for people to get comfortable with it and understand how it works.

Kristen: Would you say they need to understand how the buffers work in relation to more of a traditional life insurance product?

Marc: Exactly. And I think getting the thought of "OK is this product even more of a management tool for my client to use in a LIRP strategy?" And as that message gets out there, you might see people say "if I'm going to recommend VUL as part of a LIRP sale, this might be the better option."

Kristin: I was going to guess you would say more in the accumulation space, but that long-term death benefit guarantee also is nice even in the accumulation space, I would imagine.

Marc: It's easier to think about death benefit products first. And it's a broader market for us. But then the LIRP sale may come in after.

Jeff: And there may be a fair number of sales where — clients want the best of both worlds, right? They want the guarantee, and they want the upside accumulation. Pru's product is perfect for that.

Kristin: Who doesn't want the best of both worlds, right? So, Jeff, what sort of last thing do you think our readers need to know about these VUL RILA options?

Jeff: These new buffered accounts may be the right type of accounts during periods of high volatility. You and your clients don't have to hope that you've guessed which is the right account to be in — you can actually split up your allocation so that you can put your available premium into both buffered accounts. So no matter how the return comes out, you're covered. And you're using diversification — they say diversification is our best defense. And you can help maximize your returns during different economic cycles. So I think that's what they should focus on.

Kristin: Okay, that's a great thing to focus on. Marc, you get the last question. What about you? What do you think our listeners need to know about these new product options?

Marc: I think producers need to be looking at these and educating themselves. We're here to help with that, because I don't think these options are going away. Instead, I think we're going to see more of them. And the success that the carriers have had on the annuity side, they're going to leverage that. And in addition, when you think about where the sophistication has gone with all of these hedging strategies, it's hard to imagine that they'll back pedal and go the other way. I think carriers will regard this as a place to be creative and offer something that's unique.

So we will probably see even more creativity around these hedges, and someone will think of a better mouse trap around that. Getting yourself educated about them now, understanding generally how they work, and who's offering them. And then deciding if you are comfortable with these approaches, and whether you have enough information.

And the last point I'd say is that — we kind of say this all the time — it's important which carrier you sell with, and are they supporting it in the right way? And we've seen carriers that have excellent in force policy management tools. And as these products and these return types of structures get more sophisticated, it's good to partner with someone who has one of those, like Prudential's Life Insight. If Pacific Life chose to come out with something like this, they have a good system. Lincoln's got one. So I think that's also important, because these are complex products, and ultimately you want to be able to explain how the return works for your clients, and you might need help with that.

Kristin: Yes, that is a great point. Well, thank you both so much for joining us today. We are very thrilled to have access to experts like you guys. Thanks for taking the time to explain such a complex structure in a really understandable, approachable way.

Jeff & Marc: Thanks, Kristen.

Comments